The hardest part is getting started

3. Start investing early

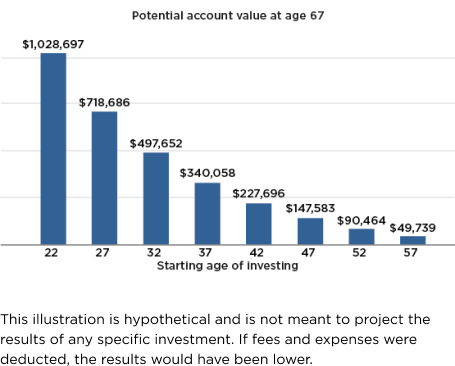

The earlier you begin saving for a long-term goal like retirement, the better off you’ll be. That’s because the sooner you start regularly adding to your account, the longer your money has to grow, thanks to a concept called compounding.

Here’s what it would look like if an investor saved $250 a month, earning an average annualized 7% rate of return on their investments.

As you can see, waiting just 5 years could make a tremendous difference in the amount you have available when you retire.

Remember, small steps have a big impact

Ready to put the “pay yourself first” idea into practice?

Enroll in your plan or increase your contributions today.